Student Loan Refinancing: 5 Benefits and Drawbacks

I graduated college with nearly $100,000 of debt. About 90% of this was made up of both federal and private student loans, while the remainder was credit card debt that helped me catch lunch between classes and keep gas in the car. Managing this debt after college, just as I was entering the work force, was an uphill battle from day one.

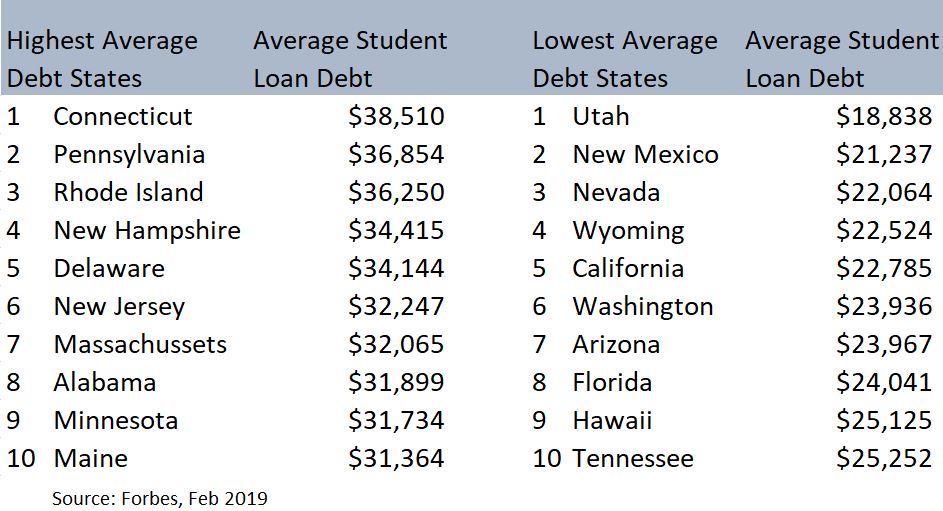

The chances are that you, or someone you are close with, may have a similar experience in trying to manage substantial student loan debt. According to Forbes, there are “45 million borrowers who collectively owe more than $1.5 trillion in student loan debt in the U.S. Student loan debt is now the second highest consumer debt category - behind only mortgage debt.”1

You’ll be hard-pressed to find a media outlet that hasn’t run multiple headline stories about the impact the student loan crisis on American life. Where you don’t find a lot of information, unfortunately, is in the realm of what individual borrowers can do about it. And more importantly what they shouldn’t do.

Student loans can either be federal loans or private loans. Private loans are provided by private institutions, such as banks. Federal loans provided by the federal government, and include various types such as Stafford, Perkins, and Grad PLUS. The context of this article is based on Federal Loans.

While it can be easy to borrow the money, paying it back on schedule is something that many postgraduates will find themselves struggling with. If your student loan debt is quickly getting out of hand, you might consider refinancing your student loans as an option. On the upside, this may help to reduce the interest you need to pay and lower your monthly cost. On the downside, things can get messy and potentially more expensive in the future.

It’s important to understand that loan consolidation and loan refinancing are technically different activities. Loan consolidation happens when you take multiple federal loans and consolidate into fewer, or just one, federal loan. Refinancing takes place when you take multiple federal and/or private loans and consolidate into one new private loan.

Check out these 5 benefits and 5 drawbacks before refinancing your federal student loan debt:

Benefits:

1. You Can Refinance Multiple Types of Student Loans Into One Refinance Loan

When financing your education with student loans, odds are you’ll utilize multiple types of loans to cover all of your expenses. Examples may include subsidized and unsubsidized Stafford loans, Perkins loans, and Direct Plus loans. Each of these will have their own payments which can make it difficult to keep up with.

When you refinance your student loans with a private lender, you can combine parent PLUS loans, federal loans, and private loans into one loan and one loan payment. This can simplify your financial life and bring a sense of ease and control to a situation that may otherwise be eternally nerve wrecking.

2. You May Get a More Advantageous Rate

While the intent of refinancing is to lower the overall cost and/or length of your loan, you can’t assume that the rate will automatically be lower than your currently held loans.

Your refinanced loan rate will be dependent on several factors, including your income, other debt obligations, and credit score. Someone several years into their career, with strong income and a good credit score, will receive a rate much lower than someone fresh out of grad school. For those with good credit and employment income, the available rates could be a huge benefit.

3. You Can Include Loans Under Your Parent's Name in Your Refinance Loan

As the price of college varies greatly, so do the resources available to individual students. You may have found yourself depending on your parents to take out student loans on your behalf. This in fact is something I had to do when I attended college.

When you refinance your student loans, you will be able to incorporate the loans your parents took out under their names. If it’s important to you to unload the burden of this debt from your parent’s responsibility, you can also choose to combine all the loans under your name and/or have your parents co-sign to help you qualify for a better rate.

4. Some Lenders May Offer Flexible Repayment Programs

Some lenders provide options for flexible repayments in the event of difficult financial situations. Examples may include forbearance on payments when you’re in school and deferment during financial hardships. Given the loss of other benefits (disability discharge, access to loan forgiveness, etc.) it may be worth finding a lender that has flexible repayments in the event of financial situations.

5. You Can Refinance Even if You Have Declared Bankruptcy

While nobody proactively seeks to be in a situation where bankruptcy is the solution, many lenders unfortunately find themselves in this situation. For those that have declared bankruptcy, you still have the ability to refinance through a private lender.

Each lender is different on their appetite for risk. Some may not accept your request at all, others may make you wait a few years before applying. Most lenders will want to see some recent activity of you repaying your debt so that they can increase their own chance of being repaid.

Drawbacks:

1. You Will No Longer Qualify for Loan Repayment Assistance

Federal loans can provide consumer protection, such as disability discharge, flexible repayment options, and access to loan forgiveness. In the event you become disabled, have an accident, or lose your job, the government may provide you with some relief.

Additionally, some jobs in public service such as professors or physicians working eligible federal, state or local public service job or 501(c)(3) nonprofit job, can receive loan forgiveness after they have made 120 qualified payments.

If you refinance your student loans, you will be turning these into conventional loans which will no longer provide these options.

2. You Will Need to Be Able to Qualify for a Traditional Loan

There is generally leeway on the requirements that underwriting uses when evaluating financial aid loans by students. As most students are in their late teens or early twenties, it’s a stretch to assume they have excellent credit in their name.

Refinancing a loan however is very different. When you attempt to refinance your loan, the loan company will require you to have a steady income, a specific debt to income ratio, and a certain level of credit score to be able to qualify. In fact, 58% of refinance applicants were ultimately rejected and those who passed had an average FICO score of 764.2

3. You Might Face Tax Consequences After Refinancing

Once you’ve refinanced your student loans, you no longer have “student loans” in your name but instead have personal loans in the eyes of the IRS. This changes the nature of the loan from a tax perspective.

If you regularly claim student loan interest as a deduction on your tax return, you will no longer be able to take this deduction. In 2019, the maximum interest you can deduct is capped at $2,500 per return (not per person).

4. You Will Lose Availability of Income-Driven Repayment Options

You may be considering refinancing your loans due to your standard repayment plan requiring payments that are too much to bear on a monthly basis. Federal loans however make other options available to borrowers.

These options include

- Income-Contingent Repayment (ICR)

- Old Income-Based Repayment (Old IBR)

- New Income-Based Repayment (New IBR)

- Pay As You Earn (PAYE)

- Revised Pay As You Earn (REPAYE)

The complexity of contingencies and characteristics of these individual repayment plans is too complex for this article; however, a point should be made that there are alternative options while staying within the federal loan system.

StudenLoans.gov provides a repayment estimator that is relatively easy to use, and provides insight as to what other repayment options may be available for your federal student loans. You can access their tool here.

5. You Will Lose Availability of Student Loan Discharge Programs

Student loans can be discharged under certain circumstances. According to the Federal Student Aid website, student loan discharge generally “refers to the cancellation of a borrower's obligation to repay some or all of the remaining amount owed on a loan due to circumstances such as school closure, a school's false certification of a borrower's eligibility to receive a loan, a school's failure to pay a required loan refund, or the borrower's death, total and permanent disability, or bankruptcy.”3

In Conclusion

Refinancing your student loans, if taken for its face value, may seem like the obvious choice if you’re looking to simplify your loan complexity, reduce the monthly payment, or get a better interest rate. There’s no question that refinancing your student loans may provide some immediate benefits.

Not all that glitters is gold however. Refinancing your loans also comes with a list of drawbacks, ranging from less tax efficiency on your interest payments to the loss of availability for income-driven repayment options.

Refinancing your student loans isn’t the only choice. Loan consolidation is also an option for federal loans, and one that should fully explored before speaking with a private lender about refinancing. Before you take the leap into any program, you should speak with a professional that works specifically with student loan analysis and repayment programs, and one that can provide you with unbiased recommendations that are specific to your unique situation. Please contact Lucid Wealth Planning LLC if you have additional questions or would like to review your situation in more detail.

1 https://www.forbes.com/sites/zackfriedman/2019/02/25/student-loan-debt-statistics-2019/#46077789133f

2 http://money.com/money/5104919/average-credit-score-student-loan-refinancing/

3 https://studentaid.gov/manage-loans/forgiveness-cancellation

Lucid Wealth Planning LLC (“LWP”) is a registered investment advisor offering advisory services in the State(s) of North Carolina and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. The presence of this article on the Internet shall not be directly or indirectly interpreted as a solicitation of investment advisory services to persons of another jurisdiction unless otherwise permitted by statute. Follow-up or individualized responses to consumers in a particular state by LWP in the rendering of personalized investment or financial advice for compensation shall not be made without our first complying with jurisdiction requirements or pursuant an applicable state exemption. All written content in this article is for information purposes only. Opinions expressed herein are solely those of "LWP", unless otherwise specifically cited. Material presented is believed to be from reliable sources and no representations are made by our firm as to other parties’ informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant or legal counsel prior to implementation. The information contained in this article is not intended to provide any tax advice. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information and should not be considered a solicitation for the purchase or sale of any security.